As budget-setting time approaches we are told that unless we agree to a huge council tax increase savage cuts in services will be necessary to balance the books.

This year has been particularly fraught with warnings that failure to approve the budget with its 16% increase in council tax could lead to members being in breach of the Code of Conduct and, in the worst case, be facing a charge of Misconduct in Public Office – a Common Law crime that carries a maximum life sentence.

Those of us with a few circuits of the block under our belts have heard it all before. I can’t remember a time when we weren’t presented with a multi-million pound “funding gap” that could only be bridged by a combination of savage cuts and above-inflation council tax increases.

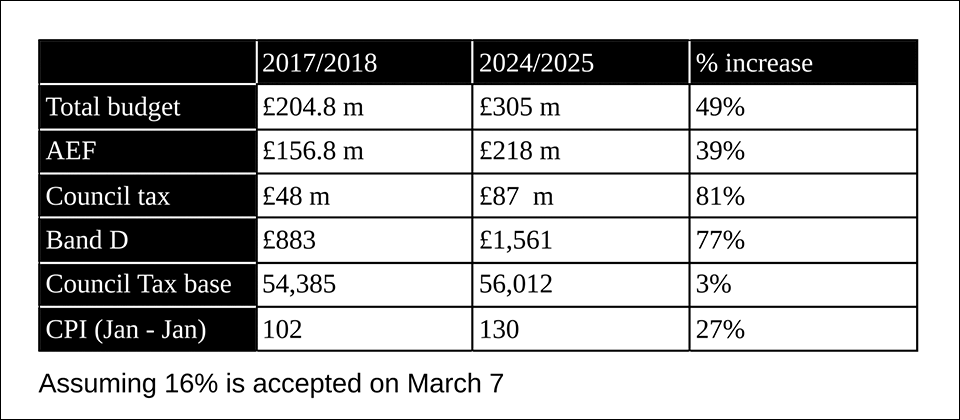

It is interesting to tabulate these movements in tax and spend over the period that the present administration has been in office (May 2017 – March 2024)

AEF = Aggregate External Funding (Welsh Government Grant).

As can be seen both spending and levels of taxation have far outrun the rate of inflation as measured by CPI figures issued by the Office for National Statistics.

For instance, council tax (both the band D rate and income) has gone up by almost three times the rate of inflation and at a time when GDP has been almost static.

Clearly, if taxes exceed GDP and inflation they consume a greater and greater proportion of the economy until there’s nothing left.

There is also some political and financial significance behind the order in which these council tax increases are imposed. Clearly there is a political advantage in having the larger increases at the beginning of the term for the simple reason that, by the time the next election comes round, there is a chance that the electorate will have forgotten about having their pockets picked.

But the real issue with the order in which the increases are introduced is the amount of money raised.

As can be seen in the table below, while the Band D rate after five years (£1249.35) is the same regardless of order , the amount of revenue raised is not.

This is a table I’ve drawn up of the increases during 2017 – 2022 – the period of the previous electoral cycle.

As can be seen the Band D rate at the end of the five years is the same (£1249.35) in all three cases, but there is a huge difference in the total amount of money flowing into the council’s coffers.

That, of course, is because the large increase in the early years is baked into all later charges.

So, if the aim is to achieve the average level of council tax in Wales (not an aspiration that I share) the fairest way to go about it is to spread the load over a number of years ( the averaging strategy in the table above) while using the council’s reserves to smooth the transition.

Finally, I should mention these so-called “funding gaps” which a bandied about as if they were real numbers.

In fact, they are based on models incorporating various assumptions about service pressures; pay rises; inflation; and the rest and, like all models they are subject to GIGO (Garbage In, Garbage Out). Not that I would describe the Director of Resources’ assumptions as garbage, but it is fair to say they are not the only ones he could have used. No doubt, as a prudent accountant, he builds a degree of caution into his prognostications. For instance the council’s medium term financial plan (MTFP) is based on the assumption that there will be zero increase in the Welsh Government’s contribution to the council’s finances over the next three years. I can’t recall an occasion in the past when this happened so it is not obvious why anyone should think it might happen in the future. However, it is a useful weapon to have in your armoury if you’re trying to persuade members to inflict a swingeing council tax increase on their constituents.