Despite a marked lack of co-operation from both Carmarthenshire and Pembrokeshire county councils, I have now managed to piece together a reasonably clear picture with regard to the Property Development Fund grant for the office block in Johnston.

The starting point is the report to PCC’s cabinet on 5 January 2015 which set out the financial aspects of the case:

Total Project Cost (exc Developers Profit)………. £790,118

Completed Project Value………………………..£318,350

Development Gap…………………………………£471,768

PDF Assistance Requested……………………. £330,375.60

PDF Assistance Recommended……………..£ 328,553.10 (45% Eligible Costs)

Note: Eligible Costs – Net Development Cost excluding ineligible expenditure and Developer Profit.

Soon after I began to take an interest in this matter, I received an email from PCC explaining that Total Project Cost should have read “inc developer’s profit” of £60,000.

However, this made no difference to the outcome because the 45% grant had been calculated on £730,000, not £790,000, though it did reduce the development gap to £411,768.

The Completed Project Value was based on a valuation dated 28 October 2014 by independent surveyors who had arrived at the value by multiplying the rental per sq ft (£8) by the floor area (3980 sq ft) and then multiplying the annual rental (£31,840) by 10 to reflect the rate of return (10%) that would be required by a prospective purchaser.

This is not as complicated, nor, as we shall see presently, as scientific as it seems.

But what it means is that, if the required rate of return was 5%, it would double the value of the building.

And if you combined a rental of £10 per sq ft with a 5% return the development gap would vanish altogether.

So, much hangs on the numbers chosen.

Indeed, just to prove that this valuation caper isn’t rocket science, on the 19 January 2015 just two weeks after PCC’s cabinet had signed off the £328,000 grant the same valuers presented another calculation based on £9 per sq ft which valued the property at £400,000.

I was also told by the council that the grant had been reduced by £22,500 and when I asked for an explanation I received the following:

I have made enquiries regarding the adjustment in grant.

The first point to note is that there was a later valuation carried out, also by Rowland Jones and dated 19 January 2015. This gave a “base valuation” of £400,000.

The second point to note is that Uzmaston Developments Ltd entered into a pre-sale agreement with Hayston Business Park Ltd.

The pre-sale Agreement Sum was £450,000. This is obviously £50,000 more than the base valuation.

Under the terms of the PDF Agreement that the Applicant was required to sign, disposal at that sale price would result in clawback of £22,500. This was calculated by applying the grant intervention rate of 45% against the uplift in value of £50,000.

Legal advice received by Carmarthenshire CC was that as they were aware of the pre-sale agreement, any PDF award should be reduced in the sum of the clawback to avoid any potential difficulties in trying to reclaim the amount from the applicant.

Not to put too fine a point on it, this explanation is rubbish.

First, it is difficult to understand the purpose of this second valuation when it had been known since 6 November 2014 (ten weeks earlier) that the property had been sold for £450,000.

Second, this further valuation from Rowland Jones was dated two weeks after the cabinet approved the grant.

Third, when the grant was signed off, the base valuation was £318,000, so, if this method of calculation is valid (which it isn’t), the uplift in valuation would have been: £450,000 – £318,000 = £132,000 and the 45% reduction would come to £59,400.

Indeed, the correct way to calculate the grant – bearing in mind the the grant mustn’t exceed the development gap – is £730,000 (eligible costs) minus the true value i.e. the amount someone was prepared to pay for it (£450,000) resulting in a maximum grant of £280,00 which is £28,000 less than the reduced figure in the council’s email.

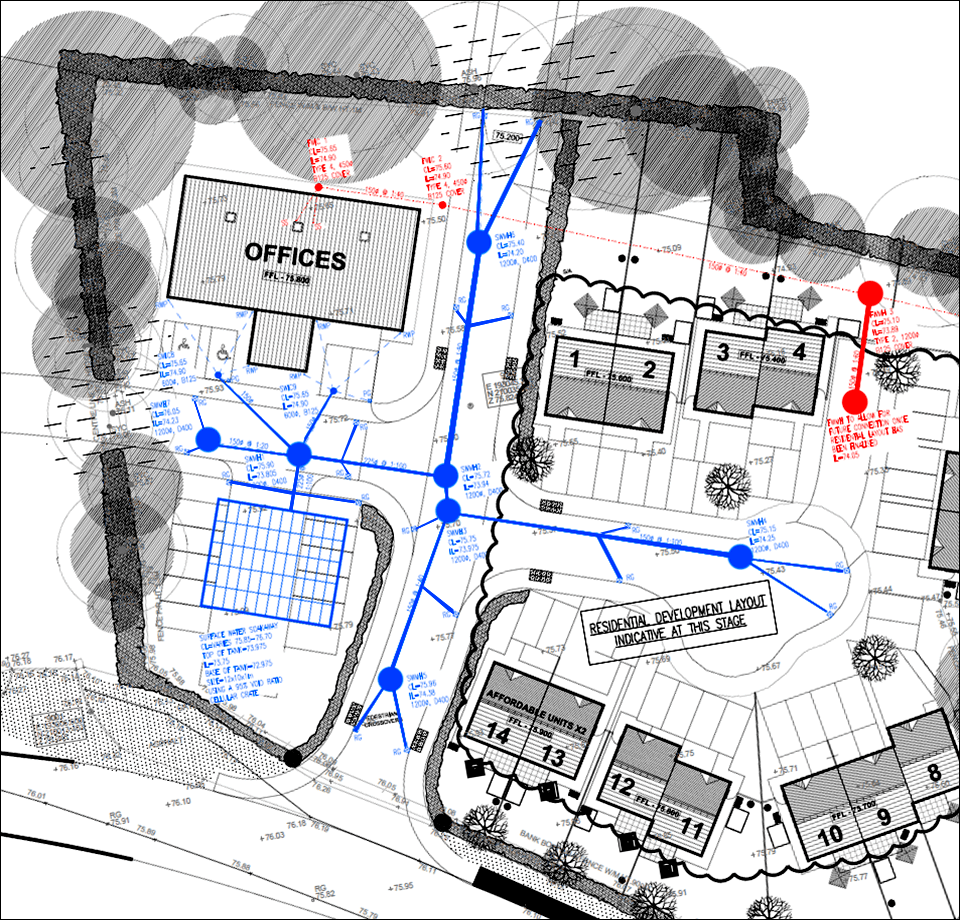

And that isn’t all because, as I showed in an earlier post, the whole of the cost (£35,000) of the drainage, including that to the adjacent housing site and the road leading to the field at the north of the site, had been loaded onto the grant-bearing office block.

At a rough guess, only one third of this was eligible expenditure, so to adjust for this the project cost, development gap, and, therefore, the grant should all be reduced by a further £23,000.

Below is the drawing that accompanied the surveyor’s valuations so it would seem that something similar may have occurred with roads and pavements (with the exception of the length of road fronting the houses).

The cost of the roadworks was £130,000 and allocating 50% to the office block and the remainder to accessing the housing development and the field to the north would lead to a further reduction of £65,000 in the grant.

So, according to my calculations, the figures should look something like this:

Total Project Cost (exc Developers Profit) £642,118 – (£ 730,118 – £23,000 (adjustment for drainage) – £65,000 (adjustment for roads)).

Completed Project Value (sale price)……..£450,000

Development Gap (and max grant)………..£ 192,000

Grant actually paid £308,000 – therefore over-payment of £116,000.

I am pursuing further lines of research on this project and will report my findings in due course.